What is an AI or Data Center Bubble?

An AI and data center bubble is a period of inflated investment, speculative growth, and large-scale infrastructure expansion centered around artificial intelligence and the massive computing facilities that support it. The core problem is a mismatch between the hype-fueled expectations and the actual utility or demand. Companies, governments, and investors pour billions into AI models and server farms with the belief that they are building the future. But the scale, speed, and justification for these investments are often untethered from reality.

What are the Defining Traits of a Bubble?

Overbuilding without demand

Corporations and utilities are constructing enormous data centers and AI infrastructure that far exceed current public, commercial, or strategic needs. Much of it is driven by forecasts and investor pressure rather than grounded analysis.Speculative capital and inflated valuations

Venture funds and major tech firms are throwing money into AI startups, chip manufacturers, and data infrastructure projects. These investments are often based on narratives and branding rather than proven returns.Resource extraction disguised as innovation

Projects consume vast amounts of land, power, and water, often in rural or economically vulnerable areas. These centers rarely deliver promised jobs or community benefits. They function as industrial resource hogs behind the marketing of futuristic progress.Techno-utopian marketing shields scrutiny

The idea that AI will transform everything justifies nearly any scale of project. Politicians and planners are told to get out of the way because “the future is coming.” This narrative silences legitimate questions about environmental impact, civic utility, or long-term consequences.Hollow applications dominate

Much of today’s AI is being used for surveillance, advertising, automation of basic tasks, and monetizing user behavior. It does not replace critical thinking, solve existential problems, or elevate public well-being. Most consumers do not see direct benefits proportionate to the scale of infrastructure being built.Risk of collapse and stranded assets

If demand fails to materialize or regulatory and public backlash halts expansion, the result is empty buildings, drained resources, and broken promises. Some facilities will be repurposed or consolidated. Many will sit idle, relics of overconfidence.

Historic Parallels

This follows the pattern of the dot-com bubble, where companies built fast without profit models. It echoes the crypto rush, where technology was sold as liberation but became a playground for speculation. It mirrors the housing bubble, where the assumption of perpetual growth justified unsustainable development.

In this case, the physical infrastructure — energy-intensive, water-dependent, and land-consuming — makes the consequences of failure far more tangible. If this is a bubble, its burst will not be just economic. It will leave scars on landscapes, utilities, local budgets, and trust in digital progress.

What Does an AI Bubble Look Like?

It would look like a rush to build capacity first and justify it later. Counties would approve huge campuses tied to ten or twenty year power reservations, water allotments, and tax breaks, even though no specific customer workloads are identified. Utilities would promise “growth” while filing for rate increases to finance new substations and transmission for facilities that produce few permanent jobs. Real estate prices near industrial zones would spike on rumor, not revenue. Politicians would pose at groundbreakings. The spreadsheets would lean on forward curves and marketing decks, not signed offtake.

It would look like resource strain dressed up as innovation. Megawatts disappear into private contracts while local manufacturers face curtailments or higher tariffs. Wells and aquifers feel the draw for cooling and dust control. Road bonds and sewer expansions get accelerated for “critical infrastructure,” then households are told to conserve. The public is told that national security or competitiveness requires silence, while NDAs and PILOT agreements keep the numbers out of sight.

It would look like hollow use cases propping up heavy concrete. Most compute would chase ad targeting, model training for marginal product features, or data hoarding with no clear civic value. Operators would talk about medicine and education but deliver inference for marketing and surveillance. Headcount on site would be a security crew, a skeleton ops team, and rotating contractors. The payroll promise would shrink after the abatement is locked in.

It would look like financial engineering outpacing engineering. Chip orders would surge, then secondary markets would fill with barely used GPUs. Developers would flip entitled land and interconnect queues for quick gains. Special purpose vehicles would refinance campuses on rosy utilization forecasts. When interest costs bite, projects would be “paused,” “sequenced,” or “optimized,” which means delayed, downsized, or sold.

It would look like political backlash and legal resistance. Neighborhoods and farm districts would organize around water rights, noise, diesel backup emissions, and line siting. Lawsuits would target defective environmental reviews, rushed annexations, and sweetheart abatements. Public records fights would multiply because basic documents are withheld as proprietary. The story would pivot from “jobs” to “grid stability,” then to “national interest,” as the benefits fail to show up.

It would end with stranded capacity and quiet sales. Some halls would go dark. Others would be consolidated by stronger operators at a discount. Counties would learn the abatement sunsets after the high load leaves. Utilities would seek to roll unrecovered costs into general rates. Officials would insist the assets can be repurposed, but the power contracts, location, and cooling design would limit alternatives.

If you want a quick field test, ask five questions.

Who is the anchor tenant, in writing?

What percent of contracted power serves public services or in-state industry?

How much water is consumed annually and from which source?

When do tax benefits turn net positive for the county?

What is the decommissioning and remediation plan with posted security?

If those answers are vague, redacted, or “competitive,” you are looking at a bubble.

Proof the Bubble has Formed

Construction Outpacing Capacity

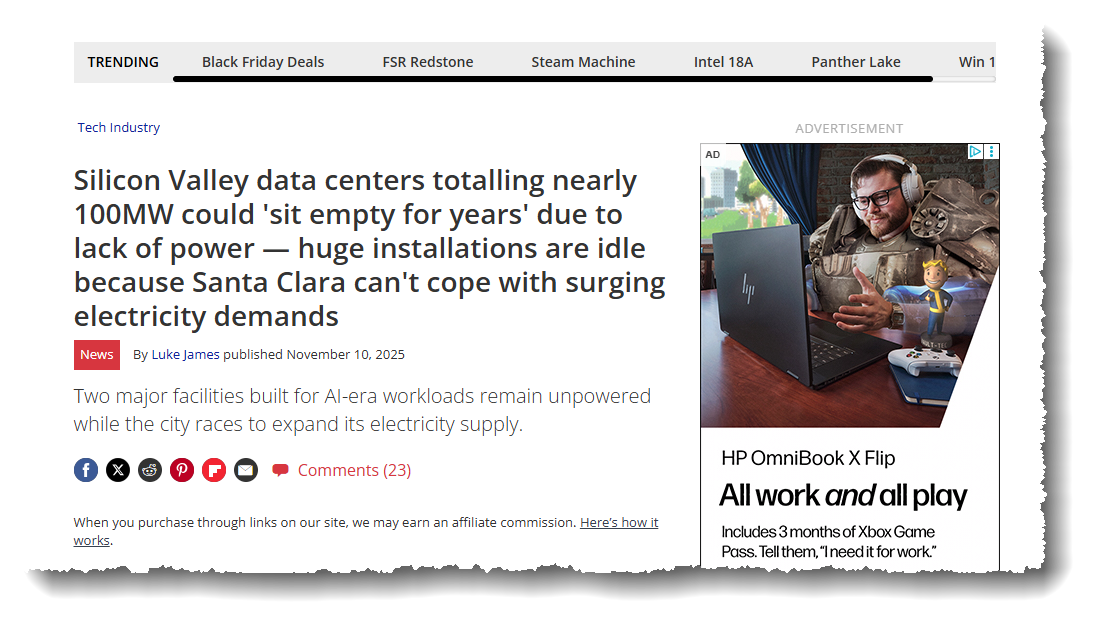

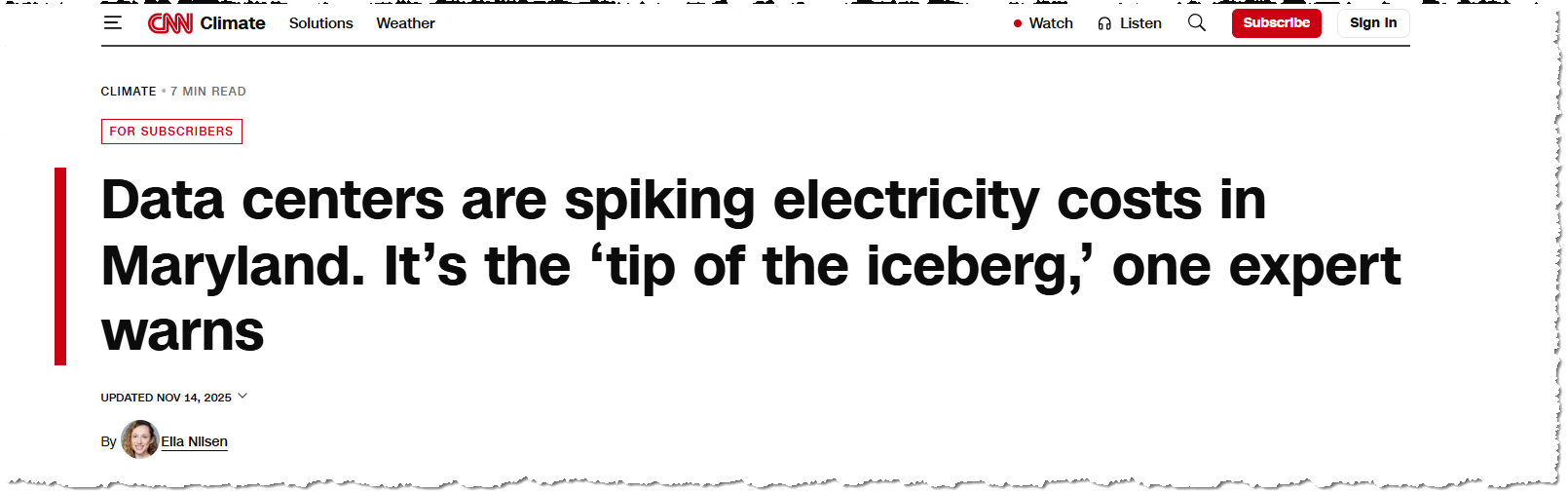

Northern Virginia’s projections are the clearest warning. Dominion says peak demand from data centers could rise to 13.3 gigawatts by 2038, up from about 2.8 gigawatts in 2022, while PJM and Virginia groups note that nearly all projected demand growth through the 2040s is attributable to data centers. Meanwhile, finished facilities in Santa Clara, California, are literally built but dark, with nearly 100 megawatts of capacity unable to energize until the local utility completes grid upgrades, a delay that could last years. Reuters and state coverage tie Mid-Atlantic bill pressure and system upgrades to the same buildout dynamics. This is not demand following customers. It is construction sprinting ahead of verified load.

Speculative capital and inflated valuations

Venture capital is flooding AI. 2025 set new records, with about $193 billion directed to AI startups and more than half of global VC dollars chasing the sector. Public markets mirror the frenzy. Nvidia briefly crossed 4 to 5 trillion dollars in market value, as hyperscalers devoted roughly 60 percent of operating cash flow to capital expenditures and bankers forecast three to four trillion dollars of AI infrastructure spending by 2030. Even bullish analysts concede that spending is running far ahead of proven monetization.

Resource extraction disguised as innovation

Where these campuses land, the resource draw is blunt. In The Dalles, Oregon, Google’s water consumption data only became public after a thirteen-month legal fight, underscoring how basic withdrawal numbers are routinely hidden. In Virginia, watchdogs and planners document multi-gigawatt campus proposals whose power needs rival or exceed nuclear output, while PJM and state groups warn that meeting this load growth keeps fossil plants and new gas capacity on the table. These are industrial footprints with heavy externalities, packaged as inevitable progress.

Techno-utopian marketing shields scrutiny

The sales pitch demands deference. Coverage from Broadband Breakfast and the Piedmont Environmental Council shows utilities and developers using sweeping economic and competitiveness claims to justify extraordinary expansions and grid upgrades, with costs socialized across all customers. In Louisiana, regulators approved new gas turbines and a $550 million transmission line to power Meta’s 4-million-square-foot campus amid public criticism over rushed approvals and thin job guarantees. When the narrative is destiny, scrutiny is treated as a nuisance.

Hollow applications dominate

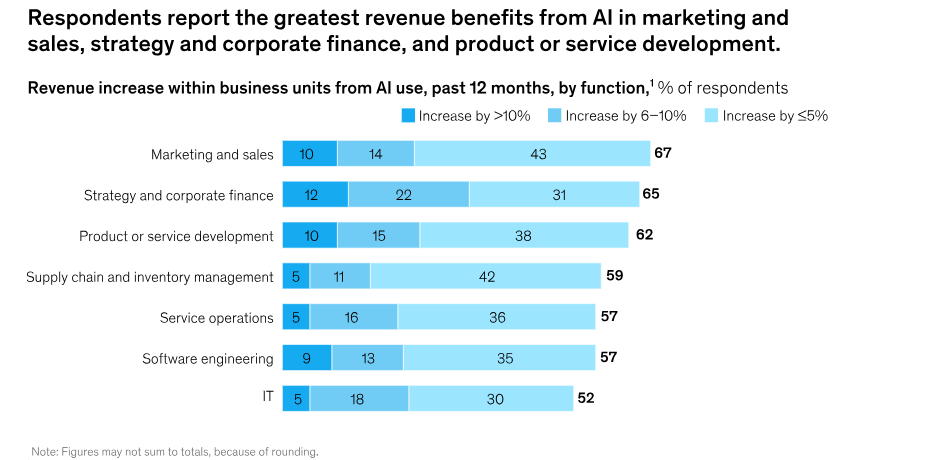

Independent market work shows where the money actually goes. McKinsey reports that the most commonly reported AI revenue gains are in marketing and sales, and that generative AI’s largest near-term lift is optimizing advertising and customer acquisition. Trade forecasts show digital ad spend accelerating, with industry groups noting rapid adoption of generative tools to crank out ad variants at scale. That is not medicine or public safety. It is targeted persuasion that demands enormous compute without commensurate civic value.

Risk of collapse and stranded assets

We are already seeing stranded concrete. In Silicon Valley, two fully built halls may sit empty for years awaiting power. Bloomberg and the Los Angeles Times detail multi-year energization delays, while Tom’s Hardware reports nearly 100 megawatts of completed but idle capacity. In PJM, Reuters ties rising bills and auction spikes to a buildout racing ahead of generation and wires. Once subsidies sunset or rates bite, weaker projects will pause, sell at a discount, or go dark.

Jobs: thin headcount after the ribbon cutting

Operators and staffing firms acknowledge the numbers. A 12 megawatt facility might run with about 20 full-time staff, and even 40 to 100 megawatt sites often employ only a few dozen. Watchdogs and recent investigations find public costs that routinely exceed a million or two per permanent job, with Ohio deals crossing the two million per job mark. That is a poor trade once construction ends.

Subsidies and abatements carry the load

A fifty-state survey by NAIOP shows at least 36 states offering exemptions or abatements, often for long periods and with modest job requirements that are hard to meet because modern sites are automated. Good Jobs First documents weak disclosure and large public costs, and Business Insider’s Ohio work finds incentives commonly topping two million dollars per permanent job. These are not market wins. They are policy-engineered outcomes.

Hardware signals of overbuying

A secondary market for top-tier accelerators is emerging. Reports show used A100 and even H100 GPUs being stripped and redeployed after policy shocks, while data center trade press now advises operators on how to resell data center GPUs to recover 60 to 80 percent of original cost. Deepening resale channels are exactly what you would expect when procurement outruns workloads.

The Boom is Real, What Happens Next?

Put together, this is not a theoretical risk. It is a visible pattern in U.S. markets right now. Multi-gigawatt forecasts and public bills, water secrecy, thin permanent headcount, rich abatements, idle finished space, and a nascent GPU resale wave are the telltale signs of a bubble forming in steel, concrete, and grid interconnects, not just on a spreadsheet.

The bust will come, what does that mean for your community and the nation?

Resources

Data center growth drives locals to fight for more say (Nov 2025)

Global data center expansion and human health: A call for empirical research (May 2025)